More than a decade after IATA launched the NDC airline standard, the question inside the travel industry is no longer “Will airlines adopt it?” but rather who can keep pace with the fastest transformation in the history of flight distribution. In 2026, the real battle among airlines, GDS providers, and agencies has narrowed to a single point: who owns the direct relationship with the customer?

In 2026, some airlines have begun offering different fares for the same flight depending on the booking channel.

A customer may see a price and ancillary services on the airline’s own website that do not appear in full within a traditional GDS screen. To the average traveler, this looks like an inconsequential technical detail. Inside the aviation industry, however, it represents one of the most significant economic shifts since the advent of electronic booking itself.

The name behind this transformation is NDC.

What is notable is that NDC is no longer the “project of the future” it was described as just a few years ago.

In many markets — particularly the Gulf and Europe — it has become, at least partially, an operational reality. Yet the industry continues to navigate a complex transition: airlines want to sell their products the way Amazon does, while a substantial portion of agencies and systems still operate with an Edifact mindset that dates back decades.

This is precisely where the central tension emerges:

NDC has succeeded technically — but its full commercial success remains unsettled.

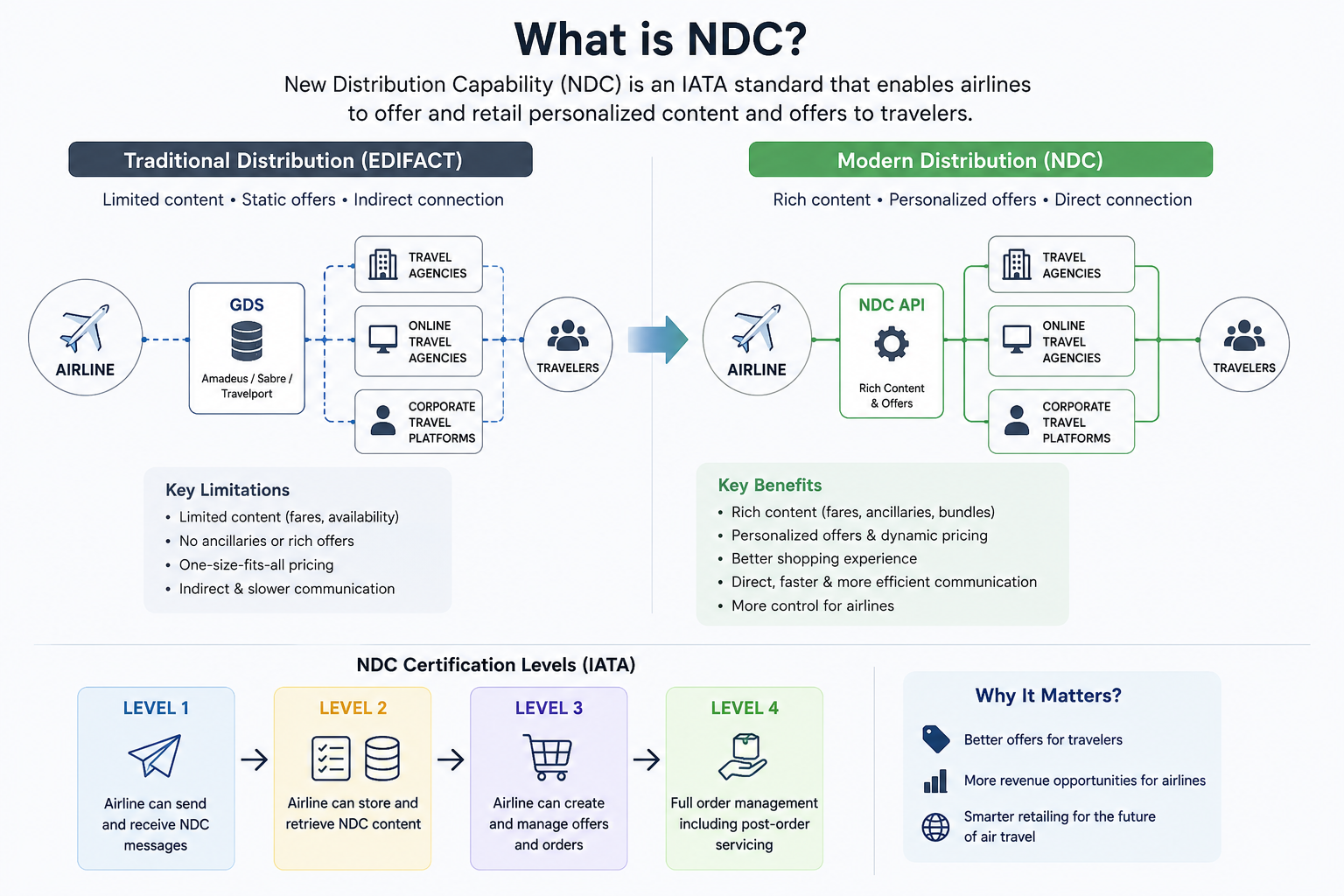

What is NDC, and why does it generate such debate?

To understand the source of this debate, one must first understand what NDC is actually trying to change.

The traditional model for distributing airline tickets relied for decades on the Edifact protocol — an effective system, but one designed for a world in which a ticket was a fixed product: a departure point, an arrival point, and a price.

The aviation industry has since changed fundamentally.

Adopting the NDC airline standard represents a significant step toward improving the booking experience and opening new horizons within the travel industry.

Airlines no longer sell only a “seat.” They sell:

- Baggage

- Paid seat selection

- Wi-Fi

- Lounge access

- Upgrades

- Flexible bundles

- Offers that vary by customer, channel, and timing

This is where NDC — or New Distribution Capability — emerged as IATA’s attempt to rebuild the entire flight sales model from the ground up.

The core idea is straightforward in theory:

give airlines greater control over their offers, pricing, and content, rather than relying entirely on the traditional GDS environment.

It is for this reason that IATA has backed the initiative since 2012 as part of the industry’s broader shift toward Airline Retailing.

The various certification levels reflect the depth of integration:

- Level 1: Basic message exchange

- Level 3: Advanced offer and pricing management

- Level 4: Near-complete support for the full sales cycle, including servicing and ancillaries

The problem, however, is that many players declare “NDC support” while the actual experience remains far removed from the full retailing concept IATA envisions.

According to estimates from Phocuswright and Skift Research, a significant share of bookings from major global airlines now flows through NDC channels to varying degrees — though full operational adoption remains uneven across markets and agencies.

Gulf Airlines: Who Is Actually Leading the Shift?

If any region embraced NDC with serious intent early on, it is the Gulf.

Emirates was among the first carriers to treat NDC as a long-term distribution strategy rather than a temporary API project. The airline expanded its partnerships with Sabre, Amadeus, and Travelport, focusing on building an environment that allows richer, more controlled presentation of its products.

Behind the technical discourse, however, a clearer message emerged:

airlines want to reclaim control over the product and the customer.

According to reports from CAPA and Skift Research, Emirates — like many major carriers — is working to reduce its full dependence on traditional channels and improve its capacity for:

- Dynamic pricing

- Ancillary sales

- Offer personalization

- Distribution cost reduction

Qatar Airways has pushed aggressively through Oryx Connect, with a clear focus on direct sales and direct connectivity. Yet like others, it has faced challenges around post-booking servicing and integration with large corporate systems and TMCs.

SAUDIA’s movement cannot be separated from Vision 2030 and the broader digital transformation underway within the Kingdom. The airline operates in line with IATA ARM directives, with incremental upgrades to its distribution environment and deeper alignment with modern retailing standards.

Etihad Airways generates less media noise, but it is among the most technically stable of the Gulf carriers in this space — particularly given its focus on the corporate segment and premium distribution.

The most telling paradox emerges at the low-cost carrier level.

flynas and Wizz Air Abu Dhabi were built from the outset on a direct-sales, digital-first model — which positions the NDC philosophy closer to their natural mode of operation than it is for traditional full-service carriers.

Put differently:

some LCCs today appear closer to the future of distribution than legacy carriers themselves.

“The question is no longer whether NDC will proliferate — but who will own the customer when the game is complete.”

The Travel Agency Dilemma: Adapt or Lose Leverage?

If airlines view NDC as an opportunity, many agencies see it as a dual threat:

- Technical

- And commercial

Large agencies and TMCs have already begun investing in:

- NDC orchestration

- Aggregators

- Mid-office automation

- New servicing tools

The picture looks markedly different for small and mid-sized agencies across the Middle East.

A significant portion still relies on:

- Legacy GDS environments

- Outdated workflows

- Non-technical teams

- Limited back-office systems

For these companies, the shift to NDC is not merely a “technical upgrade” — it is a complete rebuilding of the way they operate.

The challenges include:

- Development costs

- Training

- Exchange and refund issues

- Fragmented standards

- Divergent workflows across airlines

An executive at a regional TMC described the situation during the Travel Technology Europe conference:

“Agencies are not afraid of NDC itself… they are afraid of the operational chaos that may come with it.”

That explains why some agencies still prefer the traditional environment despite mounting pressure.

But the deeper problem is that the revenue model itself is changing.

Airlines are now able to:

- Offer exclusive fares outside the GDS

- Sell directly

- Control content

- Personalize pricing

This means the travel agency is no longer simply a “ticketing intermediary” — it is compelled to evolve into:

- A consultant

- A technology platform

- Or an integrated travel experience manager

Amadeus and Sabre: Why the GDS Did Not Disappear

Years ago, many predicted that NDC would render the traditional GDS obsolete.

What happened was quite different.

Amadeus, Sabre, and Travelport did not disappear — they reinvented themselves.

Amadeus pushed aggressively toward an NDC-X strategy, attempting to transition from a pure distribution system to an orchestration platform managing:

- Traditional content

- NDC content

- Servicing

- Mid/back office

- End-to-end offer management

Sabre focused on expanding its partnerships with Gulf airlines — notably Emirates and Qatar Airways — while working to maintain its position as the core operational infrastructure for large agencies.

Travelport, for its part, appeared to lag for a period before accelerating its investments in recent years to defend its share of the agency retailing market.

The reality is that the GDS providers understood early on that resisting NDC was not viable.

They are therefore seeking to play a new role today:

not as traditional intermediaries — but as a technology layer connecting airlines to agencies.

Yet the industry continues to grapple with:

- Inconsistent standards

- Servicing failures

- Workflow complexity

- Uneven content quality across carriers

This is what has made the full transition slower than IATA anticipated years ago.

The Next Three Years: Who Wins the New Distribution Economy?

Between 2026 and 2029, the air distribution industry appears set to enter a more decisive phase.

Scenario One: An Orderly, Gradual Transition

In this scenario, airlines and GDS providers succeed in making NDC “invisible” to the end user, allowing the new environment to operate smoothly without significant operational disruption.

Scenario Two: A Dual Market

Large carriers operate through advanced retailing environments, while thousands of smaller agencies continue relying on traditional workflows for an extended period.

Scenario Three — and perhaps the most consequential — is a transition accelerated by artificial intelligence.

As AI enters:

- Search

- Pricing

- Recommendations

- Customer service

- Offer management

The NDC architecture becomes far more logical than legacy Edifact.

AI requires:

- Richer data

- Dynamic offers

- Flexible system connectivity

These are precisely the conditions NDC is designed to create.

For this reason, the force that ultimately drives NDC adoption may not be the airlines or the GDS providers — but AI itself.

In any scenario, the years ahead appear set to determine not only the shape of distribution — but who owns the true relationship with the traveler across the entire travel industry.

Sources cited in this article:

- IATA

- Skift Research

- Phocuswright

- ATPCO

- Travel Technology Europe

- Amadeus Press Releases

- Sabre Press Releases

- Cirium

- CAPA – Centre for Aviation

- Official airline announcements